Sector allocation and security selection were equal contributors to our outperformance for the period. Our best security selection came in the Consumer Discretionary sector (Retail), and the worst selection was in Communications Services sector (Media). Despite the detracting selection in the Communication Services sector, our quarterly results were helped by being underweight that sector. Conversely our overweighted position in Financials detracted slightly on our quarterly results as the sector lagged the overall market returns.

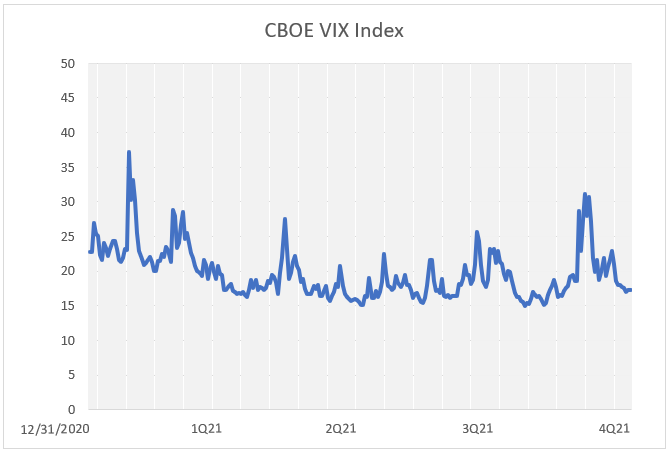

Driven by macro developments throughout the year the CBOE Volatility Index, shown on chart 1, ebbed and flowed as investors digested headlines. Despite rising volatility within the fourth quarter, returns were more evenly distributed amongst sectors than the prior periods. Seven of the eleven industry sectors posted double digit returns from both growth and defensive groups.

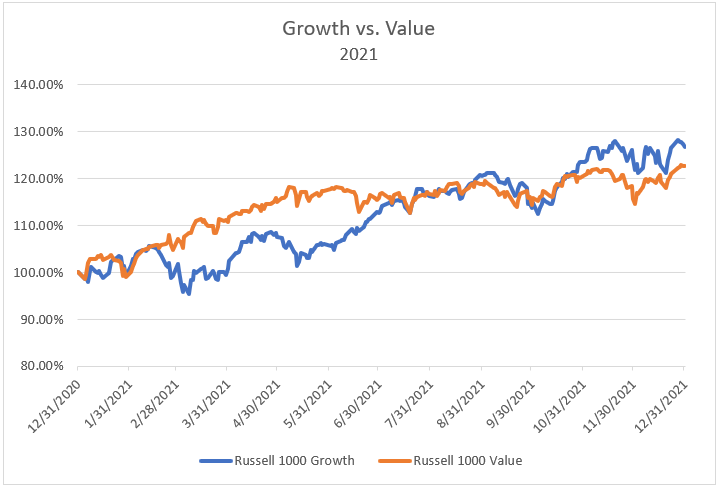

Value Rotation Faded

Mirroring the changing backdrop of volatility, 2021 was also characterized by value stocks having fits and starts of outperformance versus growth stocks. As seen on chart 2, the year opened with value stocks, specifically energy and financials, doing well before growth stocks took over leadership. The last month of 2021 saw laggards such as consumer staples and utilities lead the pack. After almost a decade of underperformance, investors are left wondering if 2022 will finally be the year where value stocks begin to outperform growth.

Chart 2

Source: Factset Research

Strong Economic, Inflation, & Earnings Growth

The economic backdrop in 2021 was supported by the strongest GDP growth since 1984. GDP growth was 6% plus in the first half followed by a slowdown in Q3 to 2.3%. When the fourth quarter results are finally released, we may see another gain of 6%, making the full year number over 5%. The economy was helped by the $3 trillion emergency stimulus, however, asset purchases from global central bank also provided financial market liquidity. Both factors combined aided economic growth.

Consumers remained strong, posting the highest net worth and lowest debt service levels on record. This backdrop led to the era coined the “Great Resignation” as record job openings emboldened workers to leave their jobs. Corporations also benefited from strong sales growth amid faster nominal growth.

Inflation Genie Out of the Bottle

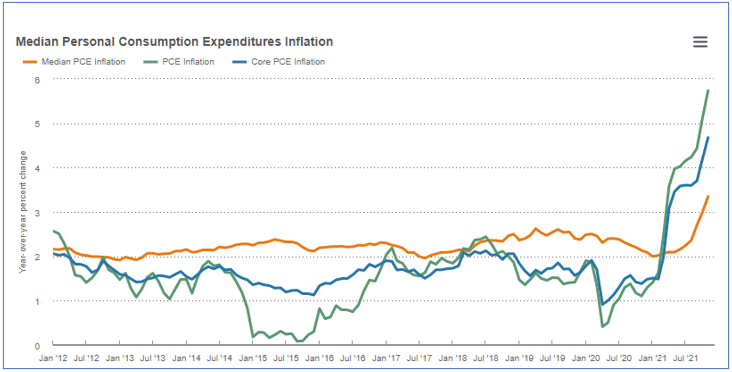

Inflation reared its ugly head in 2021 with PCE over 5% as seen in chart 3. Most people under 50 years old are likely to not recall inflation at these levels. Initially characterized as “transitory”, since certain pandemic induced segments like hotel rates and car rental prices snapped back, inflation has now broadened out towards additional goods and services.

Chart 3

Source: Bureau of Economic Analysis, Federal Reserve Bank of Cleveland, Haver Analytics

Despite the inflationary backdrop, corporate earnings have continued to surprise on the upside. At this time, companies have maintained greater pricing power to offset rising input costs. For example, IKEA just announced a 9% price hike. When all the results are in, corporate earnings may rise over 45% year over year for 2021. However, 2022 should normalize back towards the 8-9% earnings growth range.

According to S&P analyst, Howard Silverblatt, the S&P 500 index paid $14.71 per share in dividends for the fourth quarter of 20201. When compared, year over year, this per share amount increased 7.3% to equal $15.78 per share in the fourth quarter of 2021. Projections for the S&P 500 dividend growth rate is around 6.2% currently. Mr. Silverblatt went to state “the expectations are that 2022 will remain on track to set another record in dividend increases.” Additionally, 2022 should re-establish positive year over year dividend growth as 2020 was the first decline in dividends since 2009.

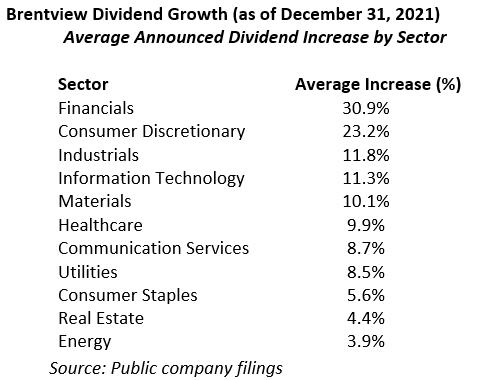

For 2021, the Brentview Dividend Growth Strategy saw 97% of our holdings pay or announce increased dividends. As seen in Table 1, Financials have led all eleven S&P sectors with the fastest growth. The average year over year announced increase of dividend payments in our portfolio currently ended the year at 14.2%.

Table 1

The rising importance of dividends

2021 was a year where value stocks started out strong but faltered after May. Will value finally win in 2022? While it will take time to determine the ultimate market rotation, we believe a barbell approach with a tilt towards value might be the best for the new year. Towards the end of 2021, we added a 3% yielding mid-cap value dividend stock from the Financials sector. While our guidelines allow for a mid-large cap range, it has been a while since we dipped into the mid cap segment.

The air in the balloon of market speculation is slowly coming out. The last few years has seen the rise of popularity from meme stocks, cloud stocks, and Bitcoin, which have all come down recently. The stock market has posted double digit returns in the last three years and the Federal Reserve is planning to take away the punch bowl, potentially muting returns.

Ultimately lower returns should make dividends a larger portion of total return. For the last three years, dividends were a small part of total return but historically have represented up to 30%-40% of portfolio returns. It’s especially important to note that during the decade of the 40’s and 70’s, dividends were 67% and 73% of total return. Both decades not only shared the significant contributions from dividends but were also decades marked by inflationary pressures.

Outlook

The expectations of three rate hikes of 25 basis points each in 2022 may not be enough to slow down the economy. It may take until 2023 before such actions have much impact. As a result, there is an outside chance that the Fed may be forced to be even more aggressive in 2022.

We continue to look for double digit growth stocks with attractive valuations. While these opportunities can be hard to find, we believe there might be opportunities within health care, financials, and industrials stocks.

In the meantime, we will continue to focus on quality companies that can absorb a correction that is inevitable in the stock market. Given our sole focus on dividends paying equities and maintaining a lower than market portfolio beta, we believe that our strategy remains well placed for today’s market environment.

1 “S&P Dow Jones Indices Reports U.S. Indicated Dividend Payments Increased $18.0 Billion in Q4 2021 and a Record $69.8 Billion in 2021” S&P Dow Jones Press Release 4 Jan, 2022

This commentary reflects the views of the Brentview Investment Management and is subject to change as market and other conditions warrant. No forecasts are guaranteed. This commentary is provided for informational purposes only and is not an endorsement of any security, sector, or index. The commentary should not be seen as a solicitation or offer to buy or sell any securities. The advisor (Brentview Investment Management, LLC), and their employees and clients, may hold or trade the securities mentioned in this commentary. Diversification does not guarantee a profit or eliminate the risk of a loss. PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS.

If you would like to learn more about Brentview Investment Management and the Dividend Growth Strategy please, click here

|

|

|