The S&P 500 index returned -4.9% in the third quarter of 2022. Volatility was the theme within the quarter as the benchmark rose 14% intra-quarter before reversing towards fresh two-year lows. With this latest quarter ending at a loss, the trend marks the third straight quarterly loss for the index, not seen since the 2008-2009 Great Financial Crisis. The Brentview Dividend Growth composite fared slightly better, posting a return of -4.8%, gross of fees. Relative to the index, Dividend Growth saw some strength from stock selection. From a portfolio positioning standpoint, stock selection within the Consumer Discretionary and Information Technology sectors contributed to our quarterly results.

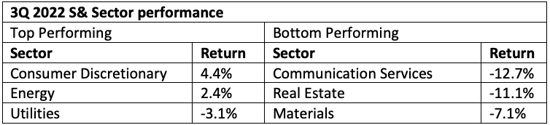

The S&P 500 index saw nine of the eleven industry sectors posting negative returns during the quarter. As seen in Table 1, the consumer discretionary sector surprisingly led the market overall. The Energy sector also did well but gave up its large gains as it peaked earlier in the quarter. The sectors that lagged in the third quarter were communication services, real estate, and materials. Even with the challenging trend of three consecutive negative quarters, the Brentview Dividend Growth composite remains well ahead of our primary index. Year to date, the strategy has returned -18.2% vs. -23.9% for the S&P 500 index.

Table 1

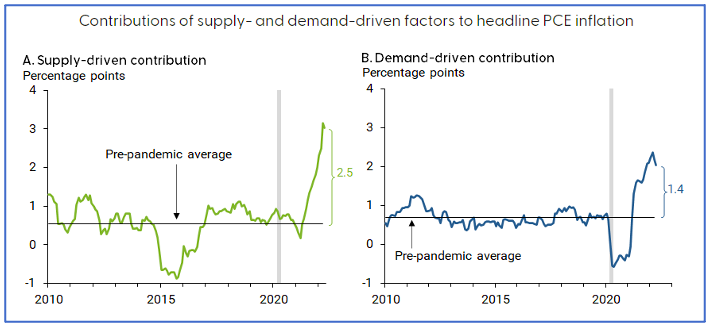

Against a backdrop of rising interest rates, the Federal Reserve is trying to rein in inflation from levels not seen for 40 years by slowing the economy. The highly regarded core personal consumption expenditures (PCE) price index remains stubbornly high. Core PCE rose 4.9% year over year in August, which followed a 4.7% increase in July. When looking at the drivers of inflation, supply chain issues represent one half of inflation while aggregate demand is only a third as shown in chart 1. Fed decisions can only influence aggregate demand which makes the job of controlling inflation even more challenging.

Chart1 Source: Federal Reserve of San Francisco

Source: Federal Reserve of San Francisco

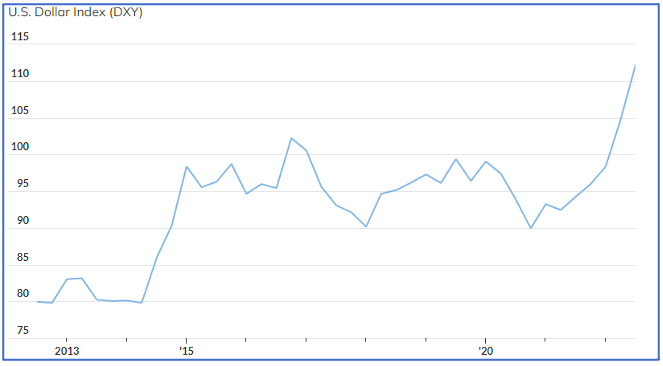

Rising interest rates in the U.S. provide the support for a strong dollar, which rose to the highest levels since 2002. The greenback was propelled 7% higher in the third quarter as seen in chart 2. The appreciation of the dollar places greater pressure on emerging market countries which have dollar dominated debt and commodities priced in dollars. It also exhibits pressure on developed countries. The Bank of Japan executed intervention to support the weak yen. The United Kingdom paused quantitative tightening to buy long term GILTS to stabilize a free-falling British pound. Historically during periods of such dollar strength, it is often a precursor of a financial or economic crisis.

Chart 2

Source: Factset Research

Source: Factset Research

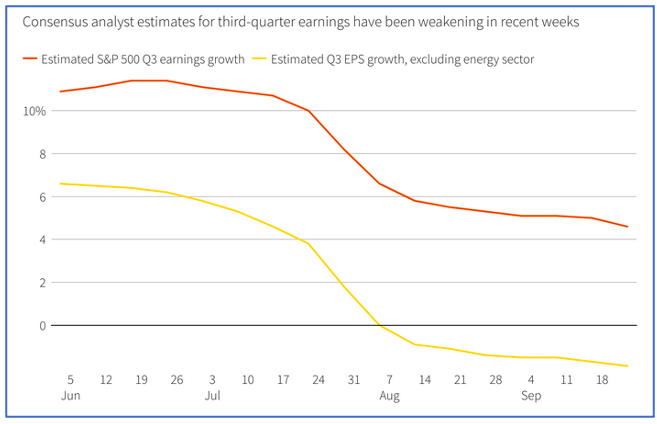

Although an official recession has yet to be determined by the National Bureau of Economic Research, latest data showed that the U.S. economy posted a second quarter of negative GDP, declining 0.6%. An economic model at Ned Davis Research shows a 98% chance of a global recession. The economic model is still showing some bright spots within the labor markets, consumer spending, and corporate profits segments. Third quarter earnings estimates are coming down from earlier double-digit estimates to mid-single digit as seen in chart 3.

Chart 3

Source: IBES

Source: IBES

Furthermore, if the Energy sector was excluded third quarter earnings would be negative overall. Currently, corporations are dealing with higher input costs and the strong dollar, which eats into earnings. A general rule of thumb is that every 10% increase in the dollar will translates into a 3% headwind for corporate earnings per share. Typically, in a recession, earnings growth turns negative on an absolute basis. As noted, earning estimates are coming down, however, they remain positive. During the quarter, economic bellwether companies, like FedEx, cut their earnings estimates and removed forward guidance altogether. It is too early to tell if this is just a company-specific problem or a trend that is going to lead to more estimates getting cut.

After three negative return quarters for the stock market what does the fourth quarter have in store for investors?

According to the Stock Trader’s Almanac there have been twelve bear markets which ended in October since World War Two: 1946, 1957, 1960, 1962, 1966, 1974, 1987, 1990, 1998, 2001, 2002, and 2011. Similarly, the stock market does well in the fourth quarter, especially in midterm election years where returns have averaged 4.2%. October is also perceived to be a bad month, especially when looking at 1929 and 1987. However, October stock market returns average 2.7% and do particularly well in midterm election cycles.

So, what could spoil this rosy outlook? An average recession can lead to equity markets seeing a peak to trough decline around 30%. At the end of 3Q, the S&P 500 Index was down almost 25%, which is still less than average. The markets appear to be following a bottoming process as an average bear market lasts 13 months and we are near month 9. When looking at longer term windows, equity valuations are off 30% from early 2002 levels as the forward 12-month PE ratio for the S&P 500 sits near 15x. This level is below the five-year average forward PE but near the average of the last 25 years. Historically, the S&P 500 forward PE ratio continued lower in three instances; March 2020, Fourth Quarter 2018, and the protracted dotcom bubble that bottomed in 2002. Taking all these observations together, volatility will likely remain. A conservative posture is warranted but timing this market could prove to be difficult.

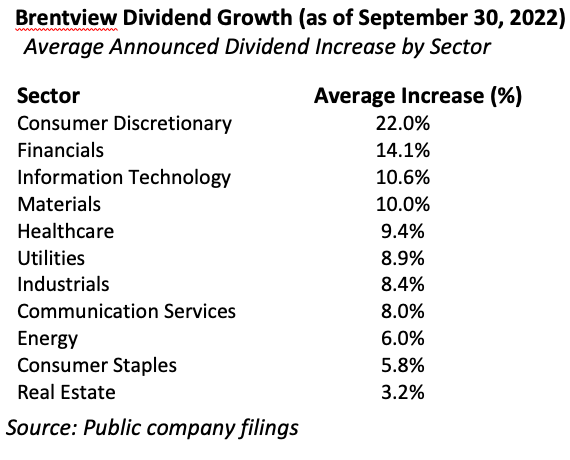

Dividend Growth Scorecard

According to Howard Silverblatt, Senior Index Analyst at S&P Dow Jones Indices, dividend cuts saw a 44.9% increase over the same period last year. Contrasting to Brentview, our strategy has not experienced a single dividend cutter during that same timeframe. Our fundamental focus has provided some clues to potential dividend cuts or businesses with potential issues. Accordingly, our fundamental research drives our current holdings but also guides the sales of stocks from our strategy.

As seen in table 1, we are very encouraged to see that 78% of our portfolio holdings (twenty-nine companies) announced dividend increases of 10.1% on average through September 30th. The companies announcing increases spanned across all eleven GICS sectors with the Consumer Discretionary sector leading with the largest announced average dividend increase to date. While dividend announcements tend to be seasonal, select companies within the information technology, consumer staples, financial, and industrial sector have yet to make any announcements so far this year. As we enter the 4th quarter, we expect to see continued dividend increase announcements from the remainder of our holdings.

Table 1

Outlook & Positioning

Broader market valuations measures suggest that we may have another leg downwards. The bottoming process is typically an occurrence that takes several months and therefore cannot be precisely timed. When the market eventually bottoms, the rebound off the lows can be quite strong, and the move will catch investors by surprise. Given these challenges, a balanced portfolio of income and growth stocks should be the safest approach.

At Brentview we focus on companies with pricing power and the ability to raise the dividend. We recently enhanced the overall income and growth potential for the portfolio to stay ahead of inflation.

When crude oil prices dipped below $80, we added to our energy exposure. Finally, we are evaluating our defensive stock holdings. We believe not all defensive sectors are alike and we expect certain defensive companies to participate on the upside when the markets recover.

We have the flexibility to own a blend of mid to large capitalization stocks. Valuations in certain sub-sectors are extremely attractive today. Furthermore, the companies that we are identifying have a 100% focus on the U.S. economy, which mitigates the risk of a global recession or strong dollar impact on profits.

This commentary reflects the views of the Brentview Investment Management and is subject to change as market and other conditions warrant. No forecasts are guaranteed. This commentary is provided for informational purposes only and is not an endorsement of any security, sector, or index. The commentary should not be seen as a solicitation or offer to buy or sell any securities. The advisor (Brentview Investment Management, LLC), and their employees and clients, may hold or trade the securities mentioned in this commentary. Diversification does not guarantee a profit or eliminate the risk of a loss. PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS.

If you would like to learn more about Brentview Investment Management and the Dividend Growth Strategy please, click here

|

|

|