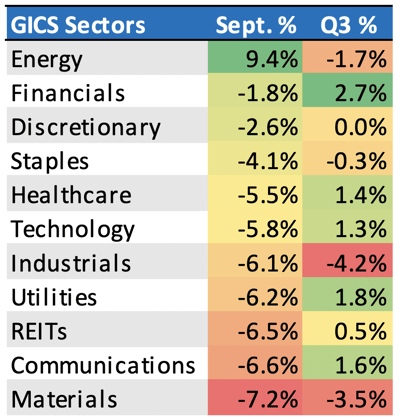

Growth stocks outperformed value stocks for the third quarter despite a strong push from value toward the end of September. As seen in Table 1, third quarter sector leaders were financials, utilities, communication services, health care, and technology. Cyclical stocks rebounded in September on fears of inflation and higher interest rates. Energy was the only positive sector in September, gaining 9.4%, aided by soaring oil and natural gas prices.

September, a month to remember

The stock market had several concerns to digest in the quarter including fiscal policy, supply chains issues, increased China regulation, the Evergrande debt fallout, and the enduring pandemic with the continued rise of the Delta variant. Related to our strategy, portfolio companies with exposure to China or those benefiting from a “re-opening economy” were the areas of detraction within the month and impacted quarterly results.

Additionally, after the FOMC meeting on September 22nd, investors became more concerned with rising interest rates and whether inflation will be more persistent than transitory. The Core Personal Consumption Expenditures Price Index saw its largest increase in June since 1991. That preceded the recession in 1992 that cost George Bush Sr. the presidential election.

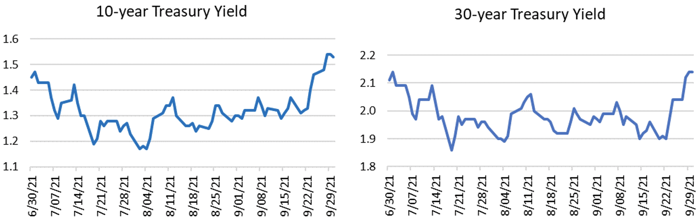

Chart 2 shows the yield histories of both the 10 & 30-year treasuries. During the quarter rates had a wide range but the 10-year treasury notes rose 8.5 basis points, their largest increase since March. 30-year treasury bond yields rose as well. The spike in yields spooked investors that the Fed may begin the tapering of treasuries and mortgage-backed securities purchases sooner rather than later. Concerns also rose that the Federal Reserve may hike interest rates earlier than expected.

Chart 2

Source: Factset Research

Earnings estimates for the S&P 500 are a key driver for market returns. Estimates have been consistently rising since Q2 2020 when analysts were far too conservative following the pandemic-induced market selloff. The S&P 500 is currently trading at 19.8x 2022 estimated earnings and 38x using a cyclically adjusted PE ratio.

We’ve seen estimates come down recently as companies struggle with supply chain issues and profit margins have been squeezed by higher costs. Plans for a higher corporate tax rate will also reduce estimates.

Goldman Sachs estimates the S&P 500 dividend growth rate for 2021 and 2022 will approach 6%. This is an uptick from the challenging 2020 period where many companies cut or omitted their dividends. According to S&P analyst, Howard Silverblatt, the S&P 500 index paid $59.25 dividends per share through September 30th, 2021, increasing from $58.85, one year earlier. This year over year growth translates into 0.60% growth of dividend cash flow. When looking at the same timeframe, using a representative account, Brentview’s year over year dividend cash flows grew 4.22%. Avoiding dividend cutters and suspenders turned out to be very impactful. To navigate 2020, a portfolio had to include sectors with consistent growth such as financials, technology, and healthcare.

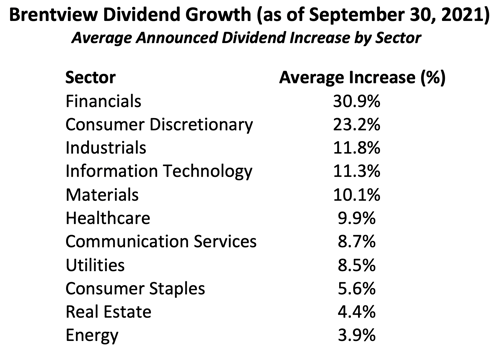

However, through the end of the third quarter, the Brentview Dividend Growth Strategy has seen 92% of our current holdings announce dividend increase so far this year. As seen in Table 2, Financials have led all the eleven S&P sectors with the fastest growth, which makes sense after being stagnant for a couple years. The average year over year announced increase of dividend payments in our portfolio currently stands 12.7% through the third quarter.

Table 2

Source: Public company filings

The Transitory Question

As we have previously mentioned in past quarterly commentaries, dividend growth, as a factor, has historically been well suited for an inflationary environment. Reason being is that companies that demonstrate consistent dividend growth tend to be businesses that have historically shown strong cost controls and pricing power. During this past quarter’s earnings releases we have seen growing recognition of rising prices . Although inflation has affected input costs on goods it has yet to have a large impact on wages more broadly. We remain comforted by the fact that long-term holdings such as American Tower, Microsoft, and Honeywell have commented on their CPI tied contracts, price increases or margin maintenance respectively.

The ongoing debate is whether inflation is transitory and how that might affect interest rates. The Federal Reserve will likely announce its taper soon without specifics on when they believe interest rates may rise. We believe the Federal Reserve will remain accommodative as they continue to purchase treasury bonds and mortgage back securities, albeit at a slower pace.

Outlook

With these crosscurrents in mind, we have navigated our investment portfolio to step up its dividend growth rate to outpace the S&P 500. We exited certain positions that exhibited single-digit dividend growth and replaced them with double-digit dividend growth stocks. A particular emphasis was on balance sheet strength and capital positions for financials stocks. We also managed to improve our ESG score with these transactions, which is a factor that some investors are paying more attention towards.

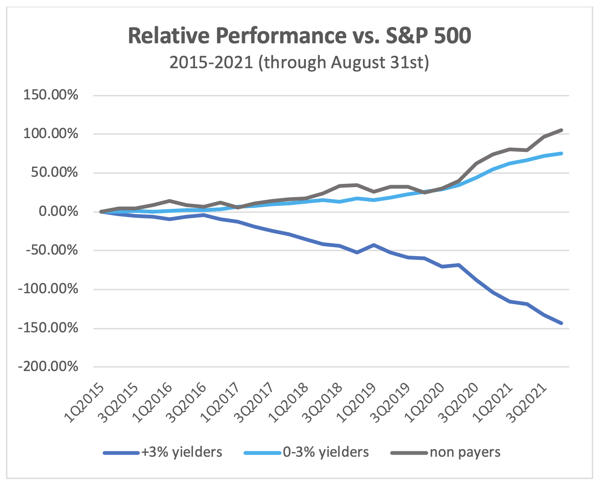

While it might be tempting in this interest rate environment, chasing yield is challenging. Our research has shown that ever since 2015, the +3% yielders have been a very difficult group from a performance perspective as seen in Chart 3. Similarly, elevated yields tend to be sector/industry specific as a particular economic sector falls out of favor. Looking at the lower yielding segment, performance has been more beneficial from a total return perspective. For this reason, we have a concerted effort to maintain exposure across the entire dividend yield spectrum. Also, we are reluctant to overreach for higher yield unless the underlying fundamentals suggest that dividend growth is sustainable.

Chart 3

Source: Factset Research, Brentview Investment Management

Source: Factset Research, Brentview Investment Management

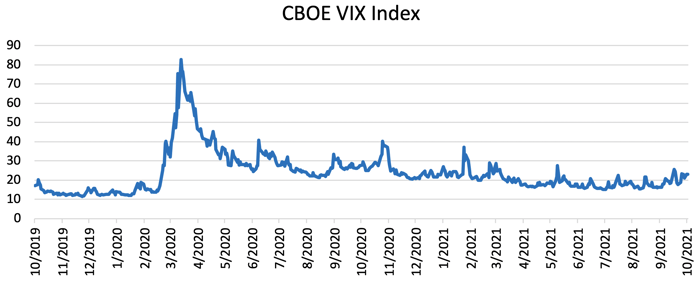

Especially in today’s environment, market volatility is something we constantly monitor. Technology stocks, traditionally higher beta and more volatile, have held up well the last 18 months during market drawdowns. This indicates to us that strong balance sheets are being recognized as a major factor in measuring company quality. These general characteristics are important to identify to help preserve capital during market drawdowns, regardless of industry sector. With these observations in mind, we believe our strategy remains well placed for today’s markets.

This commentary reflects the views of the Brentview Investment Management and is subject to change as market and other conditions warrant. No forecasts are guaranteed. This commentary is provided for informational purposes only and is not an endorsement of any security, sector, or index. The commentary should not be seen as a solicitation or offer to buy or sell any securities. The advisor (Brentview Investment Management, LLC), and their employees and clients, may hold or trade the securities mentioned in this commentary. Diversification does not guarantee a profit or eliminate the risk of a loss. PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS.

If you would like to learn more about Brentview Investment Management and the Dividend Growth Strategy please, click here

|

|

|