It is not uncommon to have guidelines within an investment portfolio. In fact, to generate repeatable results an investor should have some parameters in place to assure that an investment approach is reliable, repeatable, and consistent. However, sometimes screening methodologies are introduced to quickly eliminate companies from a broader list towards a shorter investable universe.

In this paper we discuss two of the more broadly used screening approaches when it comes to dividend investing, a minimum yield threshold and minimum years of dividend payment.

Dividend Yield Threshold

Several strategies and ETFs apply quantitative screens with arbitrary yield thresholds. For example, ETFs based on the S&P Dividend Growers Index will only be able to consider 75% of the investable universe as index rules exclude the top 25% highest yielding companies from consideration.1

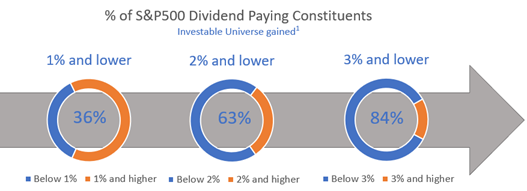

Alternatively, some active managers apply a set threshold, typically 2%, as the minimum yield a company must have to be considered for their portfolio. As seen below, as of 9/30/21, 63% of the S&P 500 dividend paying investable universe trade below 2%. A manager following this rule limits a substantial portion of their investable universe. In fact, even if a bar is lowered to 1%, a manager is missing 36% of the investable universe.

Regardless of the level, applying a dividend yield threshold omits a significant percentage of companies from the investable universe, several of which are significant market leaders and dividend growers.

Dividend History

Another popular screen is based on how long a company has been paying a dividend. Strategies can implement a dividend history requirement as few as 5 years or as long as 25 years if focused on “Dividend Aristocrats”. Companies qualifying as a “dividend aristocrat” must have over 25 years of dividend increases.2 Given this significant length and hurdle, only 65 companies qualify as an aristocrat which constitutes 16% of the 404 dividend payers in the S&P 500.

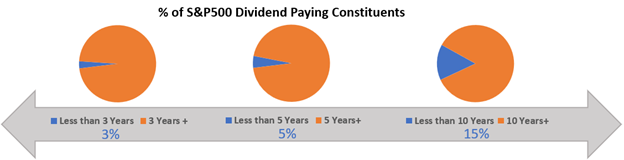

As far as active managers go, several will require 10 years of dividend history. As of 9/30/21, 15% of the investable universe have dividend histories less than 10 years. Like the yield threshold, several significant companies are omitted when applying this rule. More importantly, when applying a minimum dividend paying history rule, an investor will miss companies during their “dividend initiation” phase, which is normally a period of meaningful dividend growth and shareholder friendly ownership.

Potential Risks with Rules

To create a diversified, repeatable process, it’s important to have criteria in place. Criteria exist within a portfolio to mitigate risk and improve the chances of success. Given the changing landscape of today’s dividend payers, setting minimum dividend thresholds and dividend history timeframes are not risk mitigators. In fact, as the previous illustrations have shown, these rules likely introduce unintended risks such as sector concentrations or higher interest rate sensitivities.

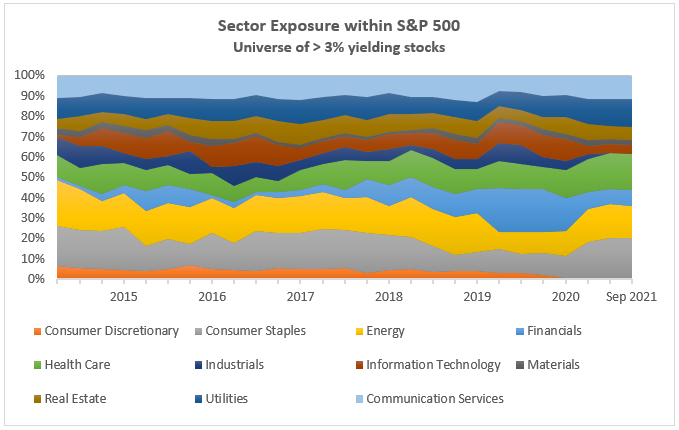

When looking at the sector concentration within a “greater than 3% universe”, a couple of risks really jump out. First, very significant benchmark sectors, like Information Technology become incredibly underrepresented. More importantly, when yield is the primary focus, slow growth/higher yield sectors are more emphasized. For example, in the chart below, Staples and Energy represented over 40% of the universe and maintained significant representation. As we have also shown in our other valued added piece titled “Looking to yield some performance alpha? Look past dividend yield alone.” this same portfolio dramatically underperformed the S&P 500 as well. All said, an investor focused on yield may take on sector concentration and performance risk because of the significant portfolio tilts.

Source: Factset Research, Brentview Investment Management Research

Conclusion

The investable universe of dividend paying equities provides several great companies and is a strong universe to draw from. To thoroughly maximize the opportunity, fundamental research is required versus arbitrary rules. Several very well-run companies will never have a high dividend yield as they are a victim of their own success via a rising stock price.

As an equity investor what should matter is the commitment to growing dividends driven by a strong and robust fundamental business. While dividend yield is important, it’s not the only factor to consider when selecting a business or building a portfolio. Yield maximizing strategies emphasize rules which may introduce other risks such as concentration risk, interest rate risk, and performance risk.

Eliminating these overly restrictive rules allows an investor to take full advantage of the dividend landscape and create a portfolio with broader economic exposure. In addition, this less constrained portfolio could potentially consider recent dividend initiators and the faster growing lower yielders. The result of this broader opportunity set could be greater performance consistency which may improve the chances of investment success over time.

Sources:

1 https://www.spglobal.com/spdji/en/indices/strategy/sp-us-dividend-growers-index/#overview

2 https://www.spglobal.com/spdji/en/indices/strategy/sp-500-dividend-aristocrats/#overview

If you would like to learn more about Brentview Investment Management and the Dividend Growth Strategy please, click here

|

|

|